Stock options are a common form of equity compensation that startup founders use as a tool to attract talent, reward early contributors, and enable others to share in the future growth of their company. In this guide, we break down the main types of stock options, how stock options are taxed, and what strategies founders should think about before issuing stock options to their service providers.

The Basics: What Are Stock Options?

Stock options are a form of equity compensation that gives the option holder the right to purchase shares of a company at a fixed “exercise” or “strike” price. If a company’s value grows, the option holder can exercise the option at the original strike price, thereby purchasing shares that already have a higher market value than what they paid.

As such, companies typically utilize options to attract and retain talent, reward early contributors, and align employee and contractor incentives with company growth.

When Do Stock Options Come Into Play?

Many founders assume they need to grant options immediately upon forming their startup, but this is rarely necessary. Prior to raising a priced equity round — when your company’s value is still at or near its nominal par value — it often makes more sense to issue restricted common stock (i.e., straight common stock subject to vesting) rather than stock options.

Before a company’s fair market value (“FMV”) materially increases, the tax and administrative burden of a 409A valuation (which sets the strike price for options) is rarely justified. At this stage, founders and early contributors can receive straight common stock for a nominal purchase price (e.g., $0.0001 per share), locking in ownership while value is low. Note: This nominal purchase price can often simply track the par value of your common stock listed in your charter document — at least in the early days of your company.

Later in the company’s development, however, the value of the shares that the company wants to grant to its service providers will increase. Let’s say, for example, a company has a fair market enterprise value of $4,000,000 and wants to make a grant of 10% of the company to a new hire. If the company makes this grant in the form of common stock, the value of the grant will be $400,000, and therefore the recipient of the grant will be taxed as if he or she was received $400,000 in cash (resulting in a tax bill that that can be around $100,000 or more!). Because most people don’t want to pay tax for shares that are illiquid and have a high risk of decreasing significantly in value, companies instead make these grants in the form of options.

Once your company raises capital (most commonly through a priced equity round) or otherwise gains significant measurable value (such as in the form of real revenue or significant development of IP), you’ll likely be in the value range where switching from stock grants to option grants makes sense. At this time, you’ll need a formal 409A valuation to support your stock option pricing and avoid running afoul of Section 409A of the Internal Revenue Code. That is typically the point when option grants become appropriate.

Note: Setting an option’s exercise price below FMV violates Section 409A of the Internal Revenue Code and can result in severe tax penalties. For the option recipient, this can mean a 20% additional federal excise tax penalty, interest on the underpayment of taxes, and sometimes other penalties. For the company, mispriced options can trigger restatement of financials, loss of 409A safe harbor status, and potential audit exposure. When the appropriate time for granting options arises in your company’s lifespan, obtaining and maintaining a current 409A valuation is critical to protect both the company and its service providers!

Understanding the Two Main Types of Stock Options: ISO vs. NSO

In the United States, stock options fall into one of two primary categories: Incentive Stock Options (“ISOs”) and Non-Qualified Stock Options (“NSOs”).

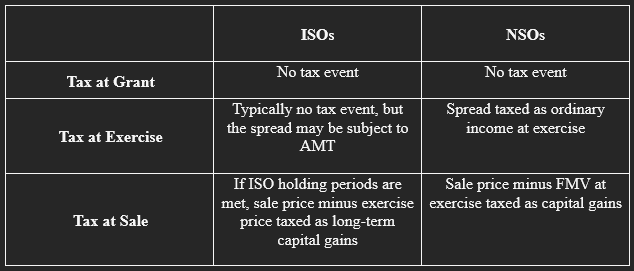

What do I need to know about ISOs?

- Restrictions on Types of Holders: Only employees may receive ISOs.

- Tax Treatment: If holding requirements are met (2 years from grant date, 1 year from exercise date), profits may qualify for long-term capital gains treatment, which usually means a lower tax rate than ordinary income tax.

- Important Highlight: Exercising ISOs can trigger Alternative Minimum Tax (“AMT”).

What do I need to know about NSOs?

- Restrictions on Types of Holders: Employees, contractors, board members, and advisors (including individuals who are not US taxpayer) are able to receive NSOs.

- Tax Treatment: The spread between the exercise price and the fair market value at exercise is taxed as ordinary income. Later appreciations are taxed as capital gains.

- Important Highlight: NSOs have fewer restrictions than ISOs, but provide generally less favorable tax treatment.

- Misclassification Warning: If a stock option that was intended to qualify as an ISO fails to meet the IRS requirements — whether due to holder ineligibility, exceeding the $100,000 annual limit, late exercise, or other issues — it automatically defaults to being treated as an NSO. While this is by no means fatal, it changes the timing and character of the taxable income. Misclassified ISOs can lead to unexpected tax liabilities for the recipient and compliance issues for the company if proper withholding and reporting were not done. As a general rule, you should always consult your legal and tax experts when granting options (and really, any form of equity compensation)!

Taxation Summary

Additional Notes for Option Recipients

- Some companies allow employees and contractors to exercise their options early, letting option holders “buy the shares” before they formally vest. This presents a number of advantages to option holders, including starting the capital gains holding period earlier. But be aware of the risks! Option holders could pay for shares that they may never fully earn or realize a benefit from if they leave before the underlying options vest or if the company itself fails.

- For options, you only need to file an 83(b) election if you “early exercise” your options and receive stock that is subject to vesting. In that case, filing the election within 30 days of exercise can lock in a low tax basis and start your capital gains holding period early.

- Companies sometimes allow for cashless exercise (or net exercise) in which a portion of the option shares are used to satisfy the exercise price in lieu of the option holder needing to exercise with available cash on hand.

Final Thoughts

For startups, issuing equity is both an essential recruiting tool and a regulatory minefield. While stock options can help attract and retain top talent, they require careful structuring and ongoing compliance to avoid costly mistakes.

By prioritizing legal and tax compliance from the start, founders can focus on what matters most: building and scaling their business. Bowery Legal can help your startup navigate the complexities of granting equity compensation so you can choose the right path for your business.